Theory and practice of the EU’s simplified trilateral trade procedure

14.10.2023

14.10.2023

Triangular trade is a type of EU trade in which a simplified tax scheme can be used for the supply and acquisition of goods between VAT-registered individuals in various EU member states. The simplified scheme can only be used if all of the legal requirements are met (Article 17 of the VAT Law).

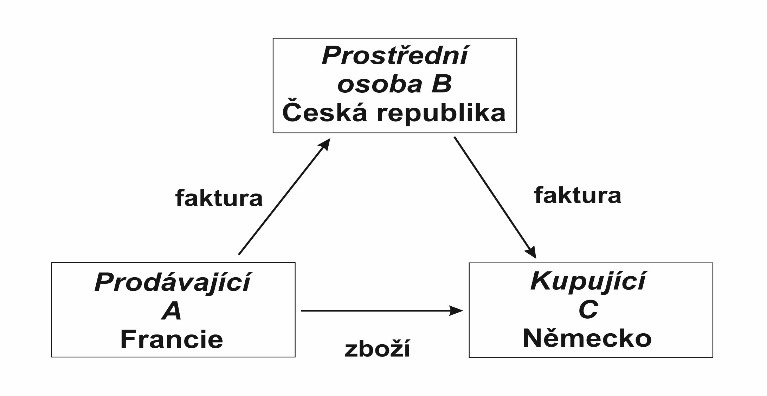

A tripartite transaction is one in which three parties (seller, intermediary, and buyer) are taxed in three distinct EU member states. This transaction comprises the supply of the same commodities by these three people, with the goods being delivered or transported straight from the seller’s home state to the buyer’s home country.

If the conditions stated by the VAT Law are met, the intermediary is excluded from the duty to declare tax in the buyer’s EU Member State under the streamlined three-way trading procedure. This duty is transferred immediately to the buyer. The benefit of this method is that it reduces administrative burden.

In a multiparty transaction, an intermediary joins the process, purchasing goods from the seller and selling them to the buyer without personally receiving them. The goods are delivered straight from the supplier to the purchaser. If the trilateral trade criteria are met, the simplified method for the supply of products inside the EU, as outlined in Article 17 of the VAT Law, may be used.

Then, using the simplified products supply technique, we will identify the many parties involved who must meet certain requirements in order to establish a tripartite transaction.

The seller in a tripartite transaction is a non-VAT exempt person registered in another EU Member State (hence referred to as JČS) from which the items are dispatched or transported.

The buyer is a person who is registered as a taxpayer in the country of JČS where the goods were dispatched or transported. In this case, the customer obtained the items from a third party (intermediary).

An intermediary is a person who is registered for tax reasons in another state (the country must be different from the seller’s and buyer’s member states). The intermediary cannot also have its registered office or branches in the same country as the customer. The intermediary buys the items from the seller in the state where the buyer is registered, with the intention of delivering them to the customer in the same EU country.

The law imposes extra conditions on the intermediary, including that he cannot register for VAT purposes in the buyer’s EU member state. If we presume that the items were transported in the Czech Republic (i.e. the buyer was registered in the Czech Republic) and the intermediary was also registered for VAT in the Czech Republic, the simplified regime cannot be used.

The acquisition of goods by an intermediary under the streamlined tripartite method and completed within the EU is tax-free if:

- Goods are purchased from another Member State via an intermediary who is not a taxable nor an identified person but is a registered tax payer in the other State.

- An intermediary purchases items in another country with the intention of delivering them to the EU’s internal territory.

- The intermediary purchased the products, directly sent or internally carried them from the seller’s Member State, and the goods were originally intended for the customer to whom the intermediary makes the delivery.

- The buyer is a VAT payer or a recognized individual.

- The buyer must declare taxes on items supplied by an intermediary as though the commodities were purchased in another state.

The intermediary, being a registered entity in JČS, is obligated to provide the seller with their taxpayer identification number and specify it in the tax document for the buyer, indicating that it is a three-party transaction.

Example 1: A taxpayer residing in the Czech Republic purchased goods from a person registered for tax purposes in Austria and then delivered them to a person registered in Slovakia. The goods were transported from Austria to Slovakia.

Solution: The Polish supplier issued an invoice to the Czech payer-intermediary. The Czech payer then issued an invoice to the Slovak buyer without VAT and indicated in the invoice that it was a three-party transaction. The Czech taxpayer reflects the purchase of goods in line 30 of the VAT declaration and the subsequent supply to Slovakia in line 31 of the VAT declaration. Then the Czech taxpayer records the supply of goods in a consolidated report under code 2.

Example 2: A Czech taxpayer purchases goods in Poland and subsequently sells them to an entity in Germany that is not registered for tax purposes.

Solution: The supply of goods to an entity not registered for tax purposes in Germany does not meet the conditions of a simplified three-party transaction.

To qualify for tax exemption when supplying goods to another country under Article 64 of the VAT Act, it is necessary for the goods to be dispatched or transported to another country.

The seller, an intermediary, or an independent third party authorized by one of them must transport the goods in order for the terms of three-party trade and VAT exemption with the right to deduct the tax to be satisfied. Thus, transportation must be attributed to the first supply of goods between the seller and the intermediary. If the transportation is done by the buyer themselves, the simplified three-party trade regime does not apply.

Example 3: A Czech taxpayer purchases items from a person registered in Poland and sells them to a buyer in the Czech Republic. The goods are delivered from Poland to the buyer in the Czech Republic.

Solution: Because both the intermediary and the buyer are registered for VAT in the Czech Republic, the conditions of the simplified tripartite transaction are not met in this case. If all other conditions are met, one of the transactions will be a purchase of goods and the other a supply of goods to the Czech Republic.

Example 4: A Czech taxpayer purchases goods from an Austrian supplier and then sells them to Italy. The Italian buyer is in a hurry to receive the goods, and the Czech payer, responsible for organizing the transportation of the goods, cannot deliver them from Austria to Italy within the 24-hour timeframe required by the buyer. Therefore, the Italian end buyer arranges external road transportation on their behalf and at their expense.

Solution: Despite complying with all other conditions of the simplified three-party transaction, the delivery of goods to Italy cannot be exempt from VAT, and the Czech payer issues an invoice to the Italian buyer, including VAT, as the buyer arranged the transportation.

Example 5: A taxpayer registered in the Czech Republic buys products from a person registered in Poland and sells them to a buyer in the United Kingdom.

Solution: Because the buyer is from a third country, the prerequisites for simplified trilateral trade are not met in this circumstance.

In-practice complications of the simplified tripartite procedure

In practice, in a multiparty transaction, the seller may carry out the transportation, satisfying the conditions of the simplified tripartite transaction, provided that all other conditions are met. The intermediary issues a VAT-free invoice to the buyer and records the transaction on lines 30 and 31 of the VAT return.

The seller and buyer, however, sometimes cannot agree on transportation, and the buyer arranges it himself. This circumstance is similar to the last one, except that the transportation had to be provided by the Austrian supplier of the goods in that case. However, because he was unable to organize transportation in a timely manner, the Italian final buyer arranged transportation on his own, at his own expense and on his own behalf.

The difficulty is that neither of these parties has alerted the intermediary, the Czech taxpayer, and he may not even be aware that the transaction does not qualify for VAT exemption; in the worst-case scenario, he will only learn about it after the tax office’s audit and assessments.

One popular approach to avoid such a problem is for the Czech payer to apply VAT as an intermediary only by producing an invoice for the supply of goods with Czech tax. Only if the buyer shows evidence of compliance with the VAT exemption provisions outlined in Article 64 of the VAT Law can the payer issue a corrected tax document and refund the VAT to the buyer.

The employment of a simplified procedure for supplying goods to the territory of the European Union in the form of trilateral trade is a right of the parties involved, not an obligation. If they have already agreed to employ this approach, they must follow all of the provisions of this section, including the correct reference on the invoice.

In practice, it has already occurred that the intermediary did not indicate in the invoice issued to the buyer that tax should be paid by the buyer, who did not pay it in practice, and the intermediary was subsequently charged VAT, because it was his responsibility to inform the buyer that he was required to pay VAT.

Legal Disputes

The EU Court has published the Advocate General’s opinion on the case C-247/21 Luxury Trust Automobile. The case pertains to the three-party trade of goods, specifically the intermediary’s obligation to correctly reference the invoice.

This concerned the three-party trade of automobiles between a British supplier (prior to Brexit), an Austrian intermediary, and a Czech end buyer. According to the Austrian tax authority, a crucial condition for the three-party transaction was not met because the invoice from the Austrian intermediary did not explicitly state that the buyer was obligated to pay VAT on the supplied goods. The invoice only mentioned that it was a VAT-exempt three-party transaction.

The Austrian tax authority assessed Austrian VAT to the intermediary, as the Austrian VAT number was used for the purchase of goods in the UK. The fact that the Czech buyer did not declare VAT in the Czech Republic and did not assert their position also played a role.

The CJEU concurred with the opinion of the Advocate General. Firstly, it affirmed that if the intermediary’s invoice does not contain the phrase “tax must be paid by the buyer,” one of the conditions for applying the simplification in three-party trade is not met. Furthermore, it stated that this condition cannot be rectified retroactively by amending the already-issued document. In practice, this means that an intermediary who issued an incorrect invoice will have to register for VAT in the country of the end buyer.

As a result, the formal requirement becomes a substantive requirement. A tax document can be corrected, but the correction will not be retroactive.

It would be interesting to observe if the Advocate General’s strict formal judgment is mirrored in the final CJEU decision. According to EY attorneys, regardless of the decision, modifications to the Czech VAT Act are expected since it wrongly characterizes the transaction between the intermediary and the final buyer.

This ruling serves as further proof that the use of VAT in international trade should not be underestimated. Every company should carefully evaluate all of its cross-border transactions to ensure that VAT is accurately imposed.

Sources:

https://www.financnisprava.cz/…ona

How to get started with 360 WEDO?

Send us the form and our specialist will contact you shortly